Weekly Outlook

What Happened This Week?

United States

● Factory activity surged, with output posting its strongest increase in four years as firms rushed to build inventories amid supply fears

● The manufacturing rebound was partly driven by “panic buying,” but the boost is expected to be temporary

● Higher energy costs pushed up business expenses and prices charged to customers

● Retail sales rose 1.7% in March, the fastest gain in over three years, largely driven by a 28% rise in gasoline prices

● Excluding gasoline, consumer spending remained solid, suggesting resilience but rising pressure on budgets

● Inflation pressures are leading companies to introduce new fees and surcharges to protect margins

● Jobless claims edged up to 214,000, while continuing claims rose slightly, reflecting a stable but slow-moving labor market

● The labor market continues to show a “low hire, low fire” dynamic, with limited layoffs overall

● Immigration restrictions have not delivered clear labor market benefits, with wage growth slowing and unemployment edging higher

● Large layoffs are becoming more accepted by investors, with some companies seeing stock gains after workforce cuts

● Political pressure on the Fed intensified, with debates around independence and the nomination of Kevin Warsh as next chair

● Warsh signaled support for rate cuts but warned persistent inflation could undermine confidence in central bank independence

Eurozone

● Manufacturing activity improved as firms accelerated orders ahead of potential shortages

● Inflation rose to 2.6% in March, driven by higher energy prices linked to the Middle East conflict

● The ECB signaled caution, with no immediate policy shift expected

● Policymakers warned that excessive government energy support could force more aggressive rate hikes

United Kingdom

● Unemployment fell to 4.9%, mainly due to fewer people seeking work rather than stronger hiring

● The labor market outlook is weakening as higher energy prices threaten growth

● The Bank of England faces a trade-off between rising inflation and a softening labor market

Canada

● Inflation rose to 2.4% in March, with gasoline prices jumping over 20%

● Industrial prices increased 2.4%, while raw material costs surged 12%, driven by energy

● Rising costs are lifting inflation expectations among businesses

● Housing market dynamics remain mixed, with slower revenue growth but resilient demand for new homes

● Homes are selling faster than listings overall, highlighting a mismatch between buyer expectations and seller pricing

Japan

● Trade data showed strong export and import growth in March, but the full impact of the Middle East conflict is not yet visible

● Energy supply risks and higher import costs are expected to weigh on growth and influence monetary policy

India

● The central bank kept rates unchanged, maintaining a neutral stance

● Policymakers warned that inflation risks remain elevated due to heavy reliance on Middle East energy and trade links

Asia (ex-China)

● Manufacturing activity strengthened as firms front-loaded orders amid supply concerns

● The Middle East conflict is disrupting energy flows to Asia, raising inflation risks across the region

Philippines

● The central bank raised its policy rate to 4.50% due to worsening inflation outlook

● Inflation is expected to exceed the upper target range in the coming years

Indonesia

● The central bank held rates at 4.75%, continuing its pause to support currency stability and manage inflation

● Policymakers remain cautious amid global uncertainty and energy market volatility

Turkey

● The central bank kept its policy rate at 37.0%, monitoring rising inflation risks from higher energy prices

● Leading indicators point to a potential pickup in underlying inflation

Global

● Manufacturing activity picked up across major economies as firms reacted to supply risks and rising prices

● The Middle East conflict disrupted key energy routes, driving up oil and gas prices globally

● Higher energy costs are feeding into inflation, increasing business costs and squeezing margins

● Supply chain disruptions and uncertainty are pushing firms to stockpile goods, distorting short-term demand trends

This Week’s Market Movers

Forex

● The USD/THB is up more than 1.50%.

● The USD/ZAR is up more than 1.40%.

● The USD/HUF is up more than 1.30%.

● The EUR/RUB is down more than 1.50%.

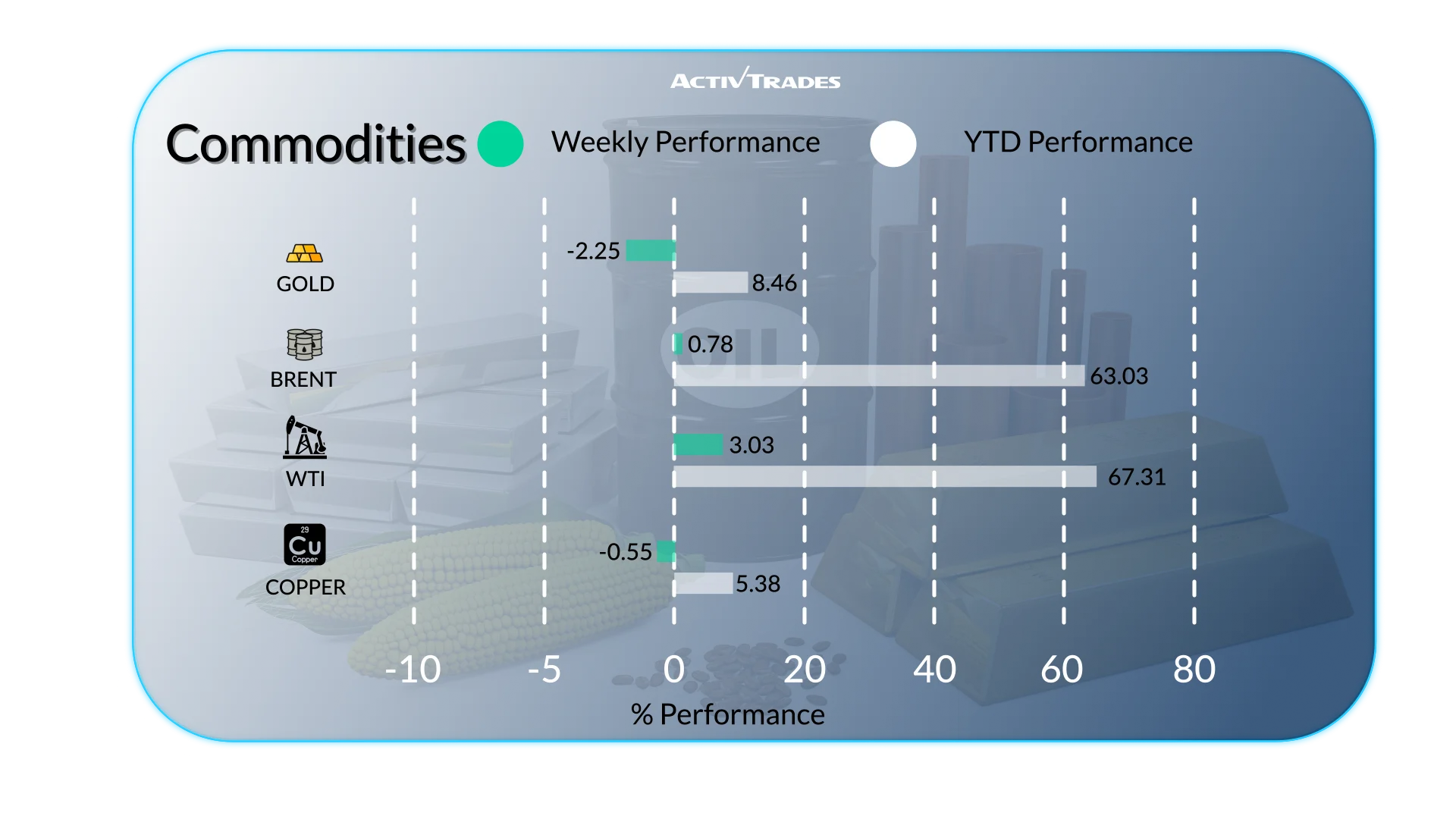

Commodities

Gold:

● London Gas Oil prices are up more than 21%.

● Heating Oil prices are up more than 17.50%.

● Brent Oil prices are up more than 16%.

● WTI prices are up more than 13%.

● Orange Juice prices are down more than 10%.

● Silver prices are down more than 8.40%.

● Palladium prices are down more than 8.30%.

Indices

● The VIX index is up more than 7%.

● The KOSPI index is up more than 4%.

● The Bovespa Composite is down more than 3%.

Shares

Tops

● ON Semiconductor: +31.49%

● Texas Instruments: +30.23%

● United Rentals: +27.96%

● ARM: +27.89%

● Marvell Technology: +25.18%

● STMicroelectronics: +23.92%

● Microchip Technology: +21.57%

● Strategy: +20.43%

● Masco: +18.55%

● Dell Technologies: +18.14%

● Infineon Technologies: +17.59%

● GE Vernova: +16.98%

● Monolithic Power Systems: +16.59%

● Analog Devices: +16.40%

● Intertek: +11.25%

Flops

● Tractor Supply: -14.70%

● Lulumon Athletica: -13.99%

● Netflix: -13.63%

● Norvegian Cruise Line: -13.50%

● Northrop Grumman: -13.46%

● Braskem: -12.65%

● Eurofins Scientific: -10.46%

● MTU Aero Engines: -10.17%

Important Events to Follow

Monday 27 April

● 06:00 AM - German - GfK Consumer Confidence (May)

○ Previous: -28.0

○ Forecast: -30

Tuesday 28 April

● 03:00 AM - Japanese - BoJ Interest Rate Decision

○ Previous: 0.75%

○ Forecast: 0.75%

Wednesday 29 April

● 12:00 PM - German - Inflation Rate YoY Prel (April)

○ Previous: 2.7%

○ Forecast: 3.3%

● 12:30 PM - American - Building Permits Prel (February)

○ Previous: 1.386M

○ Forecast: 1.36M

● 12:30 PM - American - Building Permits Prel (March)

○ Forecast: 1.35M

● 12:30 PM - American - Durable Goods Orders MoM (March)

○ Previous: -1.4%

○ Forecast: 1.3%

● 12:30 PM - American - Housing Starts (February)

○ Previous: 1.487M

○ Forecast: 1.41M

● 12:30 PM - American - Housing Starts (March)

○ Forecast: 1.4M

● 01:45 PM - Canadian - BoC Interest Rate Decision

○ Previous: 2.25%

○ Forecast: 2.25%

● 01:45 PM - Canadian - BoC Monetary Policy Report

● 06:00 PM - Fed Interest Rate Decision

○ Previous: 3.75%

○ Forecast: 3.75%

● 06:30 PM - Fed Press Conference

Thursday 30 April

● 01:30 AM - Chinese - NBS Manufacturing PMI (April)

○ Previous: 50.4

○ Forecast: 50.6

● 01:30 AM - Chinese - NBS Non Manufacturing PMI (April)

○ Previous: 50.1

○ Forecast: 50.4

● 01:45 AM - Chinese - RatingDog Manufacturing PMI (April)

○ Previous: 50.8

○ Forecast: 50.7

● 05:00 AM - Japanese - Consumer Confidence (April)

○ Previous: 33.3

● 05:30 AM - French - GDP Growth Rate YoY Prel (Q1)

○ Previous: 1.2%

○ Forecast: 1.0%

● 06:45 AM - French - Inflation Rate YoY Prel (April)

○ Previous: 1.7%

○ Forecast: 1.8%

● 07:00 AM - Spanish - GDP Growth Rate YoY Flash (Q1)

○ Previous: 2.7%

○ Forecast: 2.2%

● 08:00 AM - German - GDP Growth Rate YoY Flash (Q1)

○ Previous: 0.4%

○ Forecast: 0.5%

● 09:00 AM - European - GDP Growth Rate YoY Flash (Q1)

○ Previous: 1.2%

○ Forecast: 0.8%

● 09:00 AM - European - Inflation Rate YoY Flash (April)

○ Previous: 2.6%

○ Forecast: 2.9%

● 11:00 AM - UK - BoE Interest Rate Decision

○ Previous: 3.75%

○ Forecast: 3.75%

● 12:15 PM - European - Deposit Facility Rate

○ Previous: 2.0%

○ Forecast: 2%

● 12:15 PM - European - ECB Interest Rate Decision

○ Previous: 2.15%

○ Forecast: 2.15%

● 12:30 PM - American - Core PCE Price Index MoM (March)

○ Previous: 0.4%

○ Forecast: 0.3%

● 12:30 PM - American - GDP Growth Rate QoQ Adv (Q1)

○ Previous: 0.5%

○ Forecast: 1.5%

● 12:30 PM - American - Personal Income MoM (March)

○ Previous: -0.1%

○ Forecast: 0.4%

● 12:30 PM - American - Personal Spending MoM (March)

○ Previous: 0.4%

○ Forecast: 0.4%

● 12:45 PM - European - ECB Press Conference

Friday 01 May

● 02:00 PM - American - ISM Manufacturing PMI (April)

○ Previous: 52.7

○ Forecast: 52.5

Major Earnings Reports to Watch

Monday 27 April

● VERIZON

● Galp Energia

● Universal Health Services

Tuesday 28 April

● CMS Energy

● T-Mobile US

● General Motors

● United Parcel Service

● Starbucks

● VISA

● Mondelez

● Novartis

● BP

● BARCLAYS

● COCA-COLA

● Booking

● Robinhood

● Airbus

Wednesday 29 April

● Alphabet

● MICROSOFT

● META

● Ford Motor

● Deutsche Bank

● Regeneron Pharmaceuticals

● Chipotle Mexican Grill

● UBS Group

● Cognizant Technology Solutions

● Qualcomm

● Banco Santander

● ASTRAZENECA

● AMAZON

● LLOYDS BANKING

● EBAY

● AENA

● Adidas

● Advanced Semiconductor Engineering

● BIOGEN

● Iberdrola

● Abbvie

Thursday 30 April

● First Solar

● CATERPILLAR

● Altria

● APPLE

● Mastercard

● ING GROEP

● Amgen

● Merck

● Credit Agricole

● Eli Lilly & Co

● Banco Bilbao Vizcaya Argentaria

● BNP Paribas

● Société Générale

● AIG

● Repsol

● TechnipFMC

● Air France-KLM

● Prysmian

● BASF

● Norwegian Cruise Line

● DHL Group

● PUMA

● CaixaBank

● Altri

Friday 01 May

● Moderna

● Dominion Energy

● EXXON MOBIL

● CHEVRON

● Colgate-Palmolive

● Aon

● WisdomTree

● NATWEST

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of April 24, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.